BANKING STRUCTURE IN INDIA

CURRENT AFFAIRS

Kruthik PS

1/14/20253 min read

We often come across various types of prefixes for banks, such as Small Finance Banks, Payment Banks, Cooperative Banks, and more. Today, we will delve into this aspect and explore the banking structure in India. Let us first look at the evolution of banking structure in India, under British rule, the East India Company established three presidency banks Bengal, Bombay, and Madras which were merged in 1921 to form the Imperial Bank of India. After Independence, the Imperial Bank was nationalized in 1955, leading to the creation of the State Bank of India (SBI). Alongside these government banks, Indian banks such as Allahabad Bank, Punjab National Bank (PNB), Bank of Baroda (BoB), and Canara Bank existed, primarily focusing on foreign trade and operating near coastal trading centers.

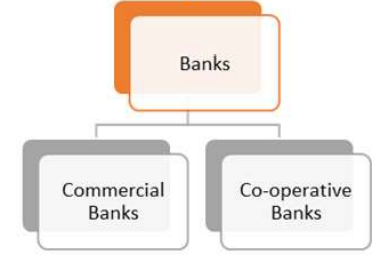

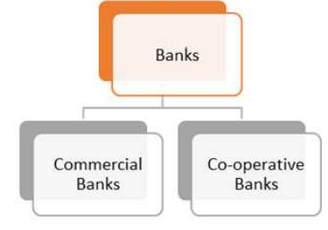

Post-Independence, many new banks emerged, primarily serving merchants and industrial houses. This created a nexus where banks provided overdraft facilities for speculative investments, often benefiting industrialists through reckless lending and boardroom ties. While these banks expanded geographically, they largely neglected rural areas, hindering financial inclusion and the achievement of Five-Year Plan objectives. After many regulatory changes today, we can broadly categorize banking structure in India in two types

- Commercial Banks

- Co. operative Banks

Commercial Banks: The main function of these types of banks is to give financial services to

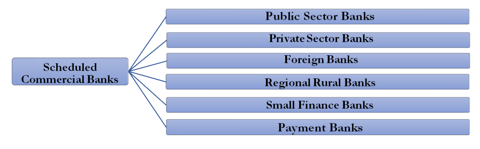

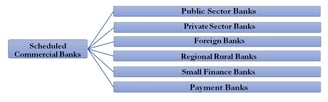

entrepreneurs and businesses. Regulated by the RBI under the Banking Regulation Act. These are the most common types of banks found in the neighbourhood and often remain in the news. These are often called as Scheduled Commercial Banks as they are included in the Second Schedule of the Reserve Bank of India Act, 1934 are scheduled commercial banks

These are the majorly following types of commercial banks viz.,

Public Sector Bank (PSB’s): These are the banking institutions in which the government, either directly or through a regulatory agency, owns most of the shares. These banks are vital to our economy because they assist rural development, encourage financial inclusion, and provide government-backed programs. Because of their emphasis on social goals and government support, they are regarded as more stable. They are considered more stable due to government backing and their focus on social objectives. The State Bank of India (SBI), Punjab National Bank (PNB), and Canara Bank are notable PSBs.

As of now, there are 12 Public Sector Banks (PSBs) operating in India. This is a significant reduction from the 27 PSBs that were functioning in 2017, following a series of mergers that consolidated them to 12 by 2020

Private Sector Bank: Private Sector Banks are financial institutions in which most of the ownership lies with private individuals or corporations. These banks are known for their customer-centric approach, innovative services, and advanced technology adoption. Examples include HDFC Bank, ICICI Bank, and Axis Bank. They primarily aim to maximize profits and deliver efficient banking services tailored to individual and corporate clients.

Foreign Banks: Foreign Banks are global financial institutions that operate branches or subsidiaries in India. These banks cater to multinational corporations, high-net-worth individuals, and trade-related financial activities. They bring international expertise and innovative products to the Indian market. Examples include Citibank, HSBC, and Standard Chartered Bank. While they focus on niche markets, their presence helps enhance competition and global connectivity in India’s banking sector.

Differentiated Banks (Small Finance Banks, Payment Banks, RRB’s): Differentiated Banks are specialized financial institutions that cater to specific banking needs or customer segments. These include Small Finance Banks, which focus on financial inclusion by serving small businesses and low-income groups, and Payment Banks, which provide basic banking services such as deposits and remittances. Examples include Paytm Payments Bank and AU Small Finance Bank. Their unique structure allows them to address gaps in the traditional banking ecosystem effectively.

Co-operative Banks:

Cooperative banks operate under licenses issued by the Reserve Bank of India (RBI) and are regulated accordingly. They are registered either under the respective State Cooperative Societies Act or the Multi-State Cooperative Societies Act, 2002. These financial institutions are owned and operated by its members, who also serve as their bank's clients. The main industries that cooperative banks assist are self-employed people, small-scale businesses, and agriculture.

Primary Cooperative Banks, often referred to as Urban Cooperative Banks, have experienced substantial growth over the years in terms of numbers, size, and the scope of their operations.

State Cooperative Banks function as an apex cooperative banking institution within their respective states. They play a crucial role in mobilizing funds and ensuring their effective distribution across different sectors. Funds are channeled to individual borrowers through central cooperative banks and primary credit societies.